Intro

This article provides a high-level, plain-language view of CBAM for manufacturers – Everything you need to know to prepare for complying with EU CBAM Regulation.

In this article you will learn:

- What is CBAM?

- Why are CBAM regulations necessary?

- How does CBAM Work?

- How do I know if I need to comply with CBAM?

- CBAM timeline: What you need to know Now, what you need to know for Later

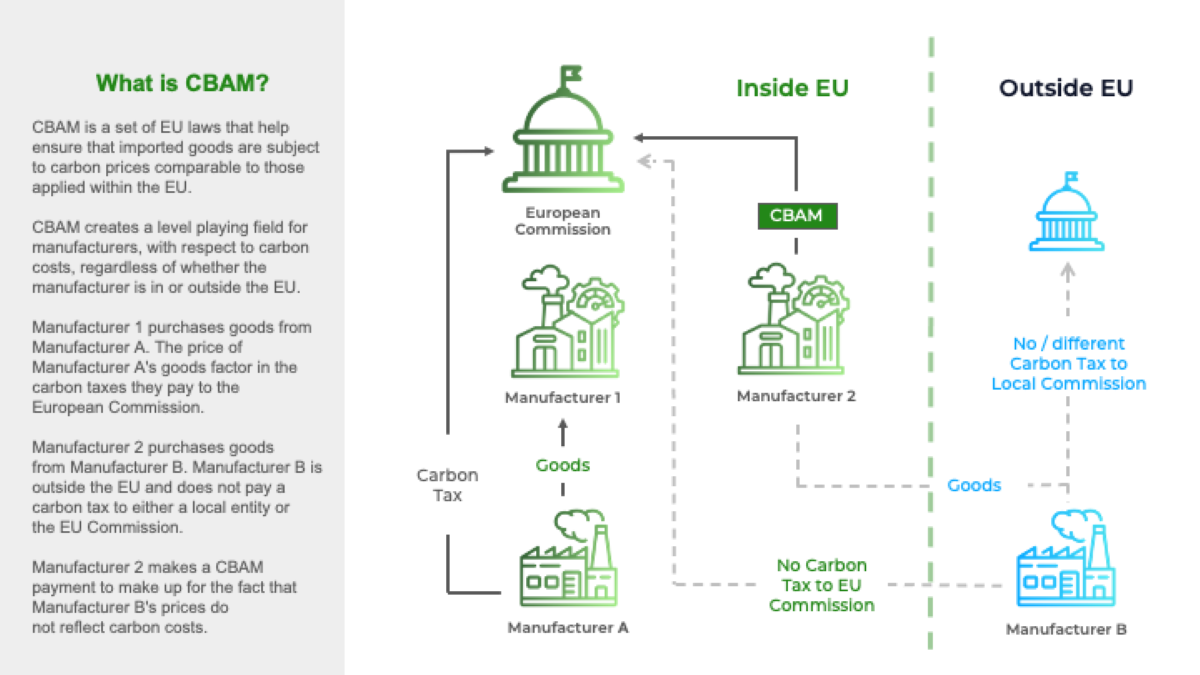

What is CBAM

CBAM is a set of EU laws that help ensure that all manufacturers consider the environmental costs of carbon emissions in their pricing – regardless of whether the manufacturer is inside or outside the EU.

CBAM stands for “Cross-Border Adjustment Mechanism”. It’s like a tax that is levied on imported goods, if those imported goods don’t face any carbon taxes in their country of origin (or the taxes they face are much more favourable).

Going forward, manufacturers inside the EU will have to track and report carbon emissions – and pay “carbon prices” for emissions based upon the EU Emissions Trading System. Because of this, prices for goods manufactured in the EU will reflect the carbon prices paid to generate the goods.

The European Commission wants to make sure that EU manufacturers are not disadvantaged in the marketplace due to the burdens of tracking, reporting & paying taxes on carbon.

CBAM helps ensure a level playing field – by requiring that importers pay a carbon price for goods manufactured in non-EU countries, if those goods don’t face carbon taxes in their country of origin, or in the case they do but they are are more favourable.

If non-EU goods don’t face carbon pricing in their country of origin, they will likely be cheaper than those produced in the EU. Requiring EU importers to make CBAM payments brings the total price of non-EU goods closer with those produced inside the EU.

Why do we need EU CBAM Regulations?

CBAM regulations help level the playing field, as far as pricing, for goods made inside and outside the EU, as discussed above.

CBAM is also part of a suite of EU regulations that, together, are meant to curb climate change.

The end goal of all the EU’s “Fit for 55” initiatives is to reduce greenhouse gas emissions at least 55% by 2030. CBAM is part of the Fit for 55 plan.

If EU manufacturers source precursor materials for their production processes from suppliers outside the EU, they may be inadvertently contributing to global warming.

CBAM for manufacturers addresses this gap and ensures that all EU manufacturing accounts for carbon emissions, regardless of their source.

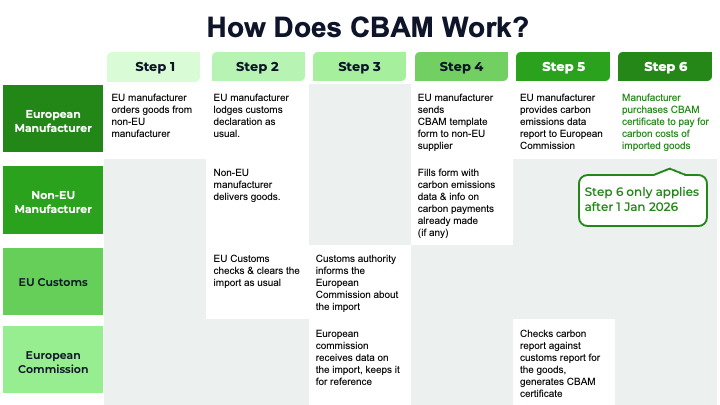

How does CBAM reporting work?

European manufacturers must track & report on all direct and indirect emissions from their production processes. This includes emissions involved with the upstream generation of precursor materials, and the downstream emissions involved with usage and disposal of their products.

For an overview of the EU’s carbon emissions reporting requirements see the Complete Guide to Sustainability & Carbon Reporting in Manufacturing.

For certain materials generated outside of the EU, manufacturers will have to provide a special type of reporting – CBAM reporting.

Under CBAM laws, importers are required to solicit carbon emissions data on imported products from their suppliers. The European Commission provides standardized forms that help EU importers ensure that their suppliers are providing the right carbon emissions data.

During the “Transitional Period” (1 October 2023 to 31 December 2025), European importers are only required to provide reporting on their non-EU goods.

After 1 Jan 2026, European importers will not only have to provide reporting, but also make payments on their imported goods’ “embedded carbon emissions”.

“Embedded carbon emissions” are the direct and indirect carbon emissions involved in the production of the imported goods.

CBAM for Manufacturers: How do I know if I need to Comply?

Not all goods imported into the EU are subject to CBAM regulations.

Only “CBAM Goods” are subject to CBAM regulations, and CBAM payments.

Here is a list of CBAM Goods:

- Cement

- Iron

- Steel

- Aluminum

- Fertilizers

- Hydrogen

- Electricity

- The European Commission provides a comprehensive listing of all CBAM goods in the CBAM Guidance

To check whether your imported goods fall under CBAM regulations, you’ll need to check if the “CN” codes (“Combined Nomenclature”, from the European Commissions’ taxation and customs union classification system) for your imported products are listed within the CBAM Guidance materials.

CBAM Timeline: What do I have to do Now?

The EU CBAM Timeline is simple:

- Transitional Period: 1 October 2023 – 31 December 2025

- Definitive Period:

- Incremental Rollout: 1 Jan 2026 – 31 Dec 2033

- Full Implementation: 1 Jan 2034 & beyond

CBAM Timeline: Transitional Period

During the Transitional Period of 1 October 2023 – 31 December 2025, importers of CBAM goods will be responsible only for the reporting of carbon emissions from imported goods.

No payments for imported goods’ carbon emissions will be required during this time. The transitional period is meant to help EU manufacturers understand the new systems for tracking & reporting on imported goods’ carbon emissions.

This period will also help the European Commission and customs offices implement tracking and document management processes.

It will also help the European Commission understand carbon pricing systems in non-EU countries, as well as embedded carbon levels involved with different imported goods.

CBAM Timeline: Definitive Period (Incremental Rollout)

From 1 January 2026, CBAM payments will be required for some imported goods.

Throughout the period 1 Jan 2026 – 31 Dec 2033, the set of goods for which CBAM payments are required will gradually expand.

For a full timeline of this incremental rollout, consult the CBAM Guidance materials from the European Commission.

CBAM Timeline: Definitive Period (Full Implementation)

From 1 Jan 2034, all CBAM Goods will require both reporting & CBAM payments.

Talk to Mavarick today about their CBAM reporting software solution.